Why a 30 year fixed is the wrong mortgage for you.

In the last few weeks, long-term mortgage rates have risen. The experts see a slowdown in the housing market. The culprit? The 30 year fixed rate.

The stalwart of the mortgage business for a long, long time. This is the entry point for Americans to buy a house no matter what program they are using. But, it’s time for it to step aside.

Because so many buyers are crying that they can’t afford a loan now, they are really kidding themselves. Yes, it is the safest thing to do. But in reality, a very large amount of loans are paid off in 7 years.

Instead of looking at today, look where you will be in 7 years. Will you move, grow your family, need to grow? Make your goal house #2.

With that in mind, start looking at long-term adjustable-rate mortgages. It is not your grandparent’s economy anymore.

The rates for the 7-year fixed based on a 30-year amortization are around what the fixed rates were a few weeks ago.

What can happen after the 7 years? It varies by lender but the rest case is a 6-2-6. That means it can go up 6 percent in the 8th year, then 2% per year and 6% over the life. Loans are usually much better than this. But, with this example, ask yourself, why would it go up 6%? That would mean we would be back in 1979, hyperinflation. If that was the case, your salary would have gone up and the value of the property increased all because of inflation.

That kind of stuff doesn’t happen anymore because the computers can adjust virtually instantaneously, there are tighter monetary rules and the internet leads the top economic minds to keep in touch every day if need be. Thanks to those who worked hard to make economic progress.

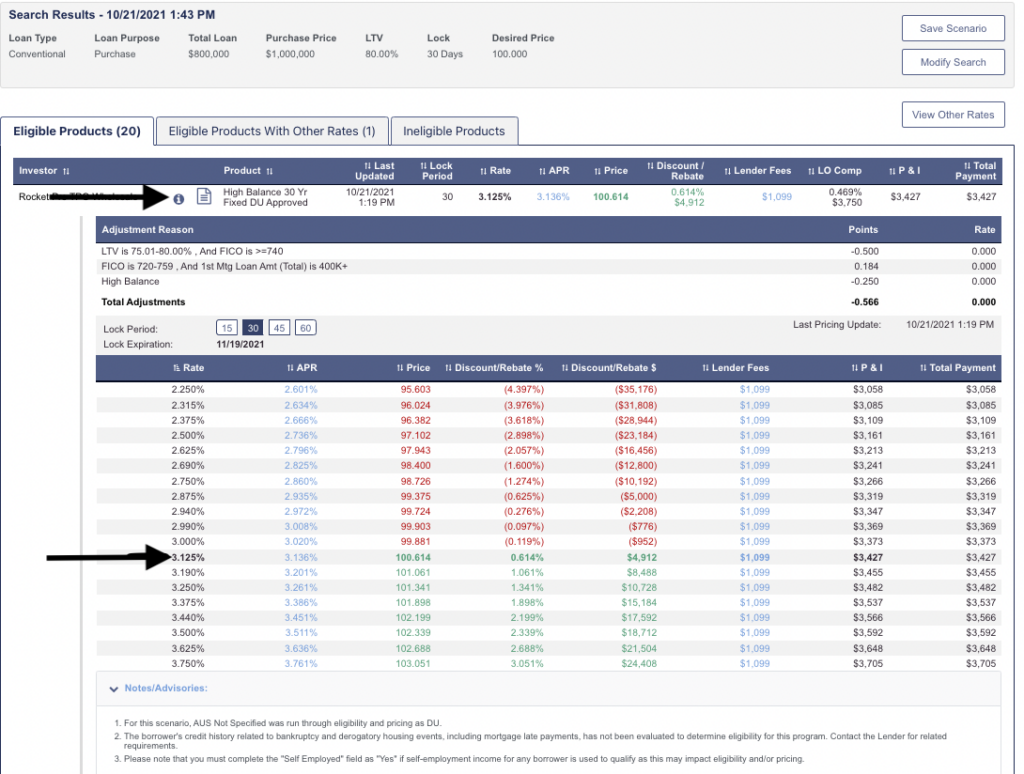

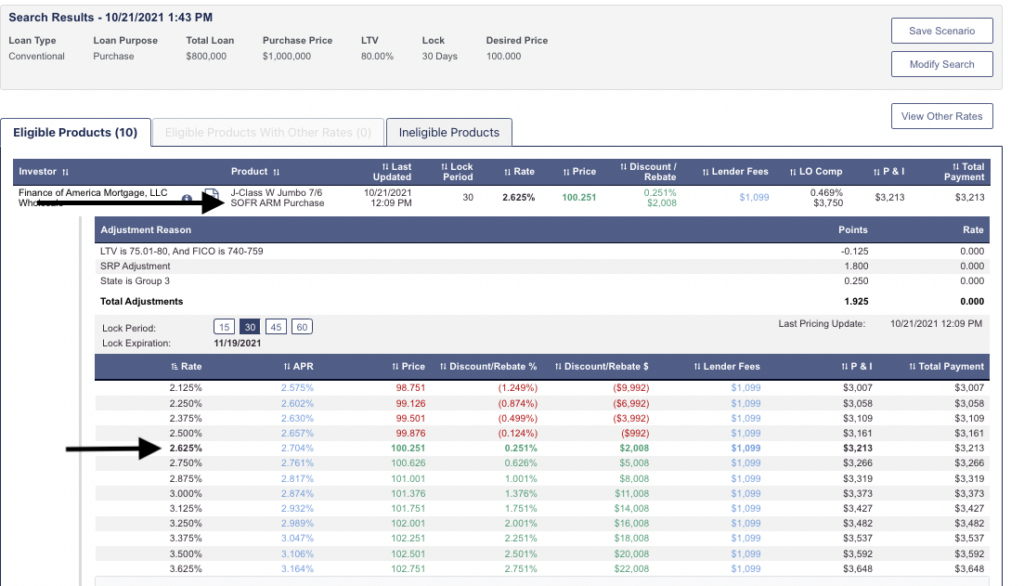

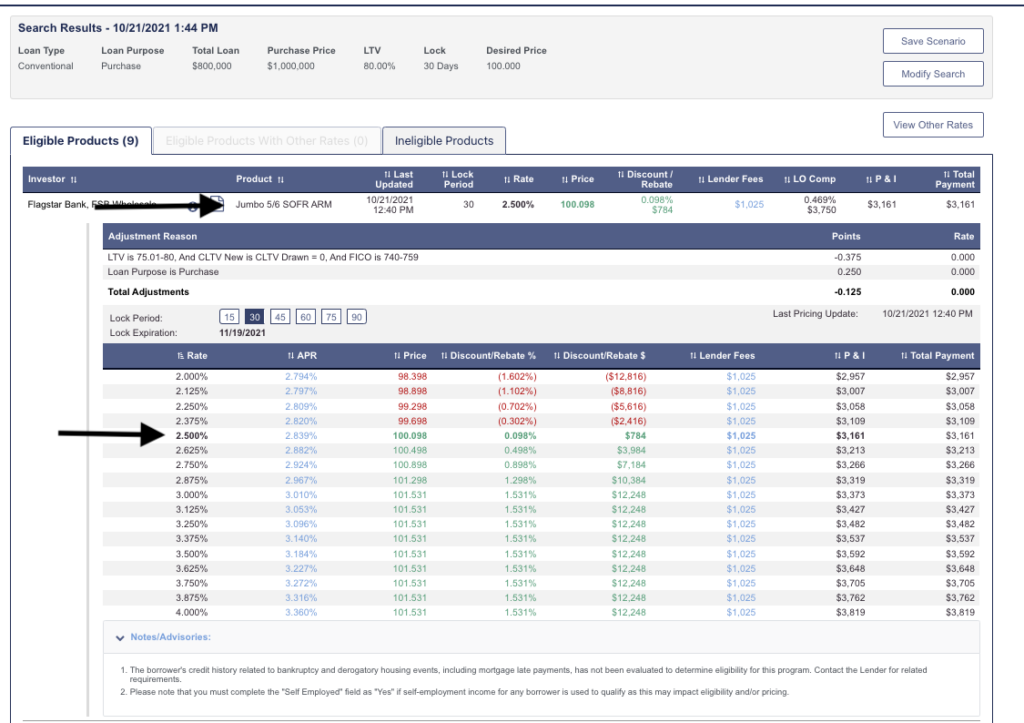

Below you will see a snapshot on October 21st, 2021 with the following scenario.

Sale Price $1M

Loan Amount $800k (within Fannie Mae)

740 credit score (that’s the max)

30-day lock

Types of loans: 30 year fixed, 10/1, 7/1, 5/1 ARMs

Rates are all the best rates available with a rebate.

30 fixed 3.125%

10/1 ARM 2.875%

7/1 ARM 2.625%

5/1 ARM 2.50%